Coffee Market: what happened last week – and where are we heading?

It is summer in the northern hemisphere. The sun is shining, a gentle breeze is blowing, the sea murmurs, the sand warms your back. Time, in theory, for a proper siesta on the beach. But the idyll is deceptive: what lies beneath is not sand but a powder keg – and both bulls and bears keep playing with matches. So much for relaxation. Nervousness rules the day at the coffee exchanges.

The geopolitical picture: barely changed. Wars and crises continue to fill the headlines, and with every passing week the market grows a little more numb to them.

At the risk of sounding like a broken record: there are, at this point, no genuinely new insights on the supply and demand situation in coffee. Picture an old-fashioned beam scale. In the bullish pan sit the tight certified exchange stocks in destination ports, the well-capitalised – and accordingly unwilling to sell – Brazilian farmers, and the prospect of a super El Niño. The still strongly inverted market, too, is a clear expression of (still) very tight coffee availability.

In the bearish pan: a delayed but most likely very large harvest in Brazil – and the selling pressure that comes with it. The delay has a side effect: Brazilian coffee will now hit the market at the same time as the new crops from Central America, Colombia and other origins. Add to this that the high prices of the past two or three years have motivated farmers around the world to plant more coffee. Larger production volumes are the logical consequence – and overproduction, as everyone knows, breeds price pressure.

Consumption, meanwhile, keeps growing – somewhat more slowly, price oblige, but steadily. Inventories around the world are remarkably empty; it will take several good harvests before the warehouses are properly filled again.

It remains, then, a tightrope walk between the bull and the bear camp. Any small piece of news can tip the scale one way or the other.

Our view has not changed: reading the market and making grand predictions is a job for prophets and gurus, and we do not believe in either. We believe in system and discipline – two virtues that hold up even in adverse market conditions. Portioned, staggered buying can help in situations like this one. Waiting and hoping is rarely a good strategy.

There is one consolation: the extreme volatility took a small summer break in New York and London last week. Compared with the week before, everything looked almost eerily calm. The powder keg, of course, is still standing there. One can only hope that bulls and bears alike put down the fuse and stop playing with fire – it is warm enough as it is, and we could all use a somewhat cooler summer break.

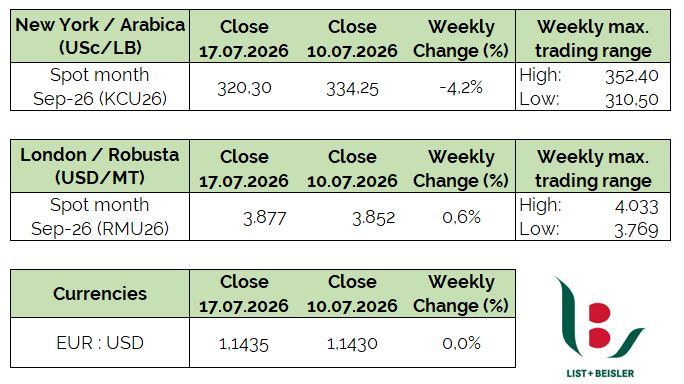

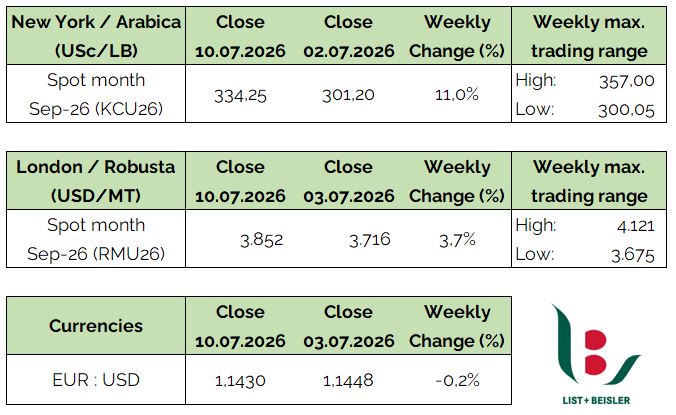

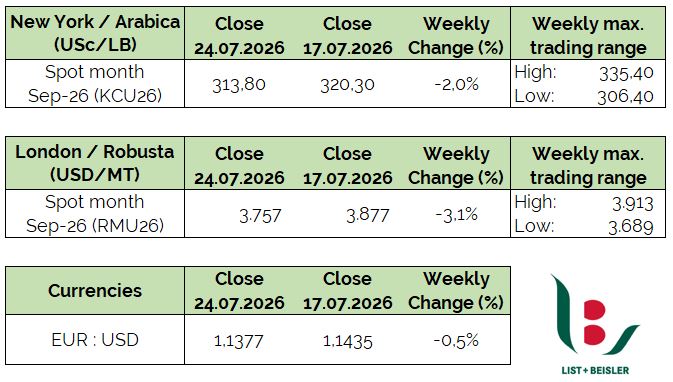

You will find the latest market developments and current prices in the table below:

Origin News: Asia Pacific

Vietnam

Vietnam is entering the hurricane season. Combined with the potential development of a Super El Niño event, there are concerns about its possible impact on coffee farms. However, rainfall has remained adequate so far, with regular precipitation across the Central Highlands supporting the healthy development of the following crop.

The market has remained relatively quiet yet firm, with an estimated 10% of the coffee crop still in the hands of farmers. Coffee exports continue to perform strongly, with July expected to be another above-average shipping month. Exporters and traders also hold more comfortable inventory levels than in the previous two seasons, reducing the risk of supply shortages ahead of the new harvest.

Operations at the Port of Ho Chi Minh are running normally.

Indonesia

Similar to Vietnam, there are concerns about the potential impact of a Super El Niño event in Indonesia, which could exacerbate drought conditions and put crops, including coffee, at risk. Currently, weather conditions across Sumatra and Bali remain relatively wet, while East Java is experiencing drier conditions.

The Robusta harvest is in full swing. Coffee continues to arrive in Lampung; however, flows are expected to begin declining in the coming weeks.

India

Following intense monsoon rains that caused flooding in northern India, authorities reported at least 50 fatalities and more than 70,000 displaced people. The heavy rainfall caused the Brahmaputra River to overflow, flooding villages across the state of Assam.

Regarding coffee, India is currently between harvests. Despite a slower start to the season, the southwest monsoon is now bringing adequate rainfall to the country's main coffee-growing regions, with overall conditions remaining favorable.

With the arrival of the monsoon season, the monsooning process for certain coffees is now underway in India. During this process, beans are exposed to moisture-laden monsoon winds in well-ventilated warehouses along the India's south-western coastal belt. The process takes approximately 12 to 16 weeks and significantly transforms the beans: they swell to almost double their size and develop a pale golden color. In the cup, monsooned coffees tend to be full-bodied, with lower acidity and often exhibit grassy, woody, and earthy notes.

There are no significant updates from the ports of Cochin or Mangalore.

Papua New Guinea

The coffee harvest in Papua New Guinea is currently underway, with overall crop conditions remaining stable. As new-crop coffees reach the market, exports are progressing well.

Due to the country's remote location and longer shipping routes, transit times may be longer than other origins.

Production Estimates in Asia Pacific