Coffee Market: What Happened Last Week – and Where Are We Heading?

Sometimes the most important news is that there is no news. The themes in the coffee world remain the same: there is enough coffee – just not where it is being consumed.

Heavy rainfall is delaying harvests by several weeks, prolonging the perceived supply drought. Certified exchange stocks continue to decline, as do available inventories in consuming countries. The moment a container touches the quay, it is loaded onto a truck and dispatched to a roaster. Coffee is almost constantly on the move these days – because hardly anyone can afford to let it sit idle.

But Brazil's new crop is on its way. Its sluggish flow to market should become increasingly noticeable over the coming months and, by then at the latest, add downward pressure to prices. Just a few weeks later, the new Arabica crops from Colombia, Central America, East Africa and Indonesia – particularly Sumatra – will begin. The Robusta harvests in Vietnam and Uganda are also only around three months away. Across all these origins, substantial investments have been made in coffee farms over recent years.

Perhaps it is the summer mood, but in our mind's eye, a small wave of coffee is beginning to form on the horizon. The emphasis, however, is firmly on "small". The coffee market has been deeply inverted for almost three years – a daily and painful reminder of just how tight inventories in consuming countries remain.

As before every wave, the beach initially appears particularly dry: the water recedes before returning with force. That is precisely the picture we are seeing in the coffee market today. Stocks in consuming countries continue to fall, while the next crops are gradually building across the origins. The great unknown remains the possibility of an approaching Super El Niño – and what impact it might have on the coming harvests.

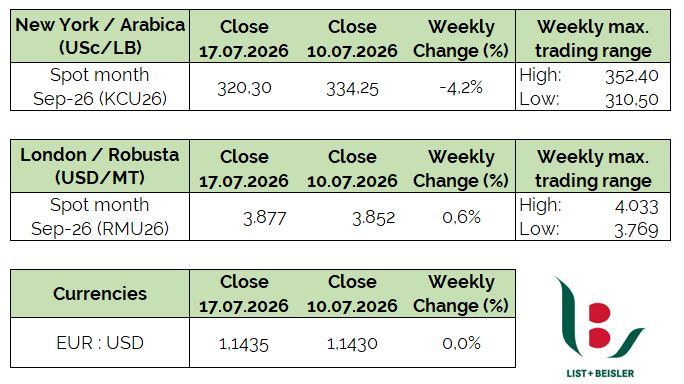

Until then, the market remains nervous. Intraday volatility continues to be exceptionally high. This was once again evident on the New York Arabica market last week: daily trading ranges were enormous, while opening and closing prices ended up surprisingly close together. Plenty of movement, in other words – but remarkably little distance travelled.

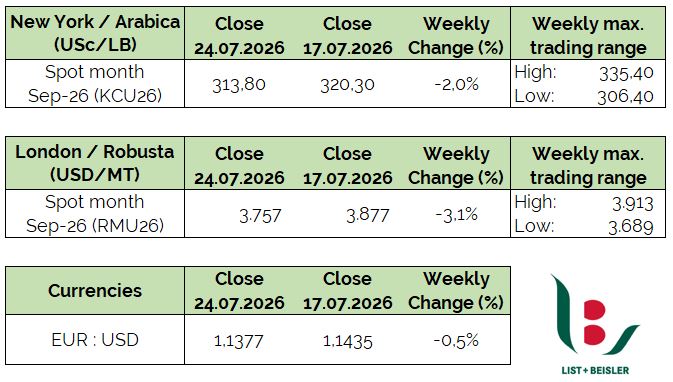

The KCU26 Arabica spot contract closed the week at 332.10 c/lb, up 5.8% on the week. Robusta displayed a similar intraday pattern but remained virtually unchanged week on week. The RMU26 spot contract closed at USD 3,782/MT.

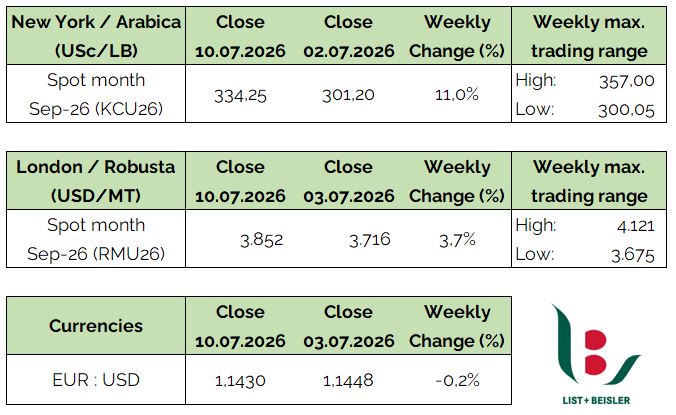

You will find the key figures in the table below – updated weekly, as always.

News from Origin: Brazil, Colombia, and Peru

Brazil

Concerns over the potential impact of El Niño weather pattern remains high in Brazil. According to the U.S. Climate Prediction Center, this year's El Niño is expected to be one of the strongest in more than 75 years, increasing the likelihood of extreme weather events such as floods, droughts, and significant temperature fluctuations. These conditions may affect coffee production not only in Central and South America, but also across parts of Asia.

In Brazil, El Niño is expected to disrupt the coffee crop's biological cycle, particularly during the flowering period in the second half of 2026. Excessive heat and irregular rainfall can result in uneven or incomplete flowering, leading to inconsistent cherry ripening. This may negatively affect quality while also making harvesting more difficult and less efficient.

Jan Walter, Managing Partner at L+B, is currently in Brazil. He reports that the harvest is ongoing and around 60% complete, although it remains behind schedule due to persistent rainfall. The wet conditions, which have continued since the harvest began in May, pose a risk to quality by making the drying process longer and more challenging. Fortunately, the weather forecast points to improved conditions over the coming week, which should support the Arabica harvest. On the Robusta side, harvesting is drawing to a close.

Market conditions remain tight, with only limited stocks available.

Logistical challenges also persist at the Port of Santos, where congestion and limited container availability continue to delay shipments. In addition, the late harvest means exports are getting underway later than usual

Views of Fazenda Vila Boa in Carmo da Mata. July 2026.

Views of Fazenda Vila Boa in Carmo da Mata. July 2026.

Colombia

Abelardo de la Espriella is scheduled to be inaugurated as the 43rd Constitutional President of Colombia on Friday, August 7. Ahead of the inauguration, the incoming administration has already announced several policy measures, including plans to cut diplomatic ties with Cuba and Nicaragua and close 15 consulates as part of a broader overhaul of Colombia's foreign service. The reforms are aimed at reducing public spending and redirecting resources towards priorities such as security, healthcare, education, and infrastructure.

Weather conditions remain a key watchpoint, with forecasts continuing to indicate rainy conditions across main coffee-growing regions.

Meanwhile, the mitaca (fly crop) harvest across central coffee-producing regions, including Antioquia, Caldas, Risaralda, and Valle del Cauca, continues to progress, with the peak now having passed.

Ongoing market volatility continues to limit coffee flows. FOB exporters remain cautious following a challenging mitaca and uncertainty surrounding the impact of weather conditions on the upcoming main crop. Nevertheless, demand remains stable for both nearby shipments and forward contracts.

There are no news in the logistical front.

Peru

After some attempts she finally made it: last week, right-wing politician Keiko Fujimori was sworn in as President of Peru, during an inauguration ceremony held at the Peruvian Congress. The new administration will serve a five-year term through 2031, adding to the growing number of right-leaning governments across Latin America.

Meanwhile, the weather outlook has improved significantly, with forecasts indicating warm and dry conditions across key coffee-growing regions, including Cajamarca, Piura, Ayacucho, and San Martín. This follows a period of erratic rainfall that had slowed harvesting and drying activities.

The local market remains tight, with limited availability continuing to put pressure on the domestic market. Although the recent market rally has encouraged some producers to release coffee, many continue to hold back stocks in anticipation of higher prices.

On the logistics side, operations are running normally at the Port of Callao.

Production Estimates for South America